Your 2027 property tax reform impact report. Four quick questions. One PDF.

Answer four quick questions and see exactly how the proposed CGT and negative-gearing changes will hit your investment property. Compare personal, trust, company and SMSF outcomes side-by-side, then weigh selling before reform against holding longer. Plain English, statutory references, no seller-side spin.

$49 per property report · pay per report, not per structure

Free exposure check

How 1 July 2027 changes your CGT

- 50% CGT discount

- Marginal rate

- No 50% discount

- Indexed gain only

- 30% minimum tax floor

Free preview only. The full report compares six ownership structures, CGT reform exposure, two sell dates, cashflow and adviser questions. See the full report.

New here

Claim your 3 free reports

Sign up and we'll add 3 report credits to your email - enough to run your first property across every structure and both sell dates.

What you get

The 2027 property tax reform breaks the old assumptions.

One report pulls timing, debt, income, structure, sale year and trust settings into a single plain-English comparison - across every ownership structure and two sell dates. This is a real one; scroll through it.

Inside every report

Current law vs proposed reform side-by-side

Annual cashflow forecast

CGT exposure with 30% minimum-tax floor

Negative-gearing restriction impact

Trust minimum tax check (proposed)

Risk scores: reform exposure, cashflow pressure, compliance

Two-sell-date comparison

Plain-English warnings with statutory references

PDF, CSV and JSON export

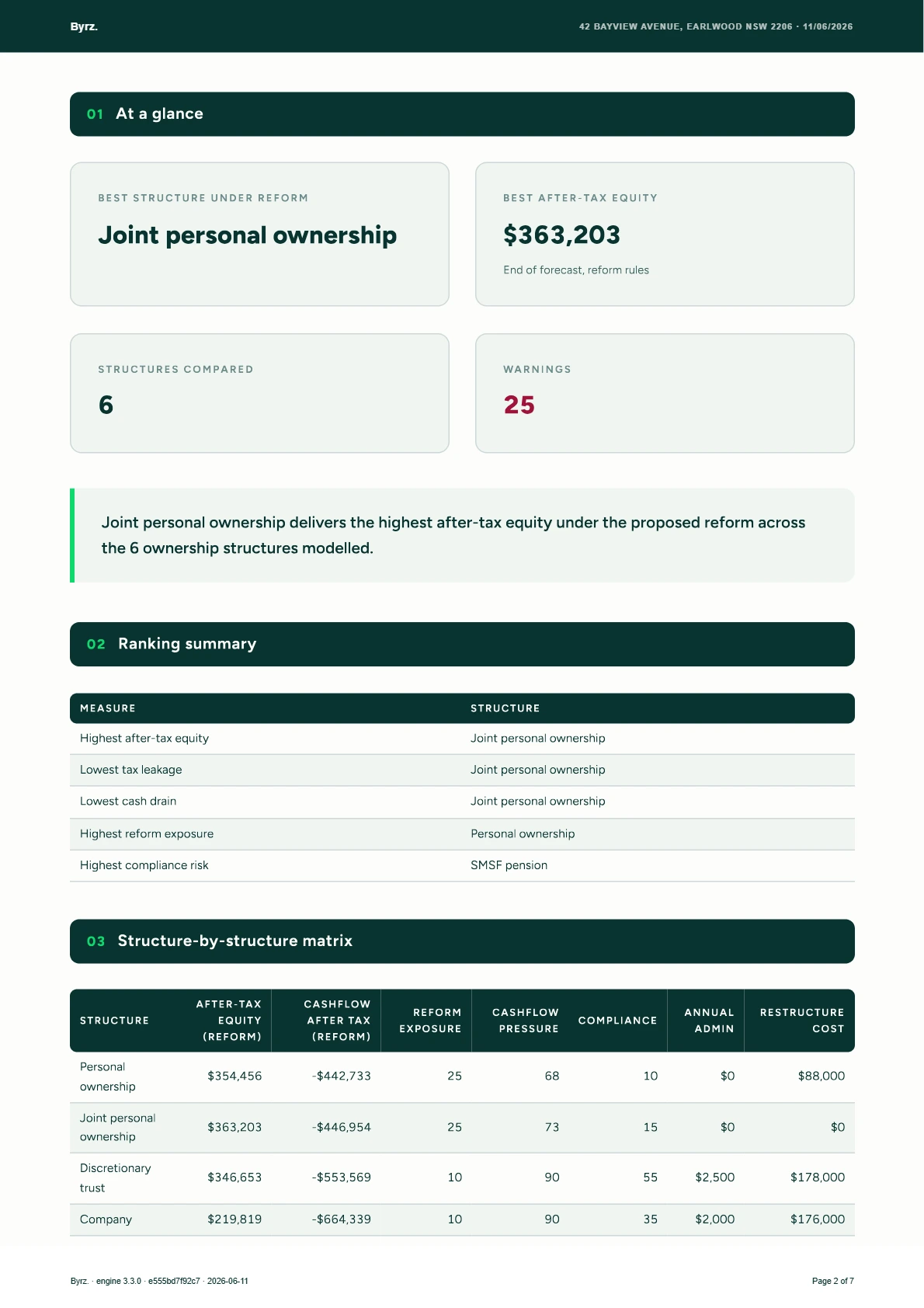

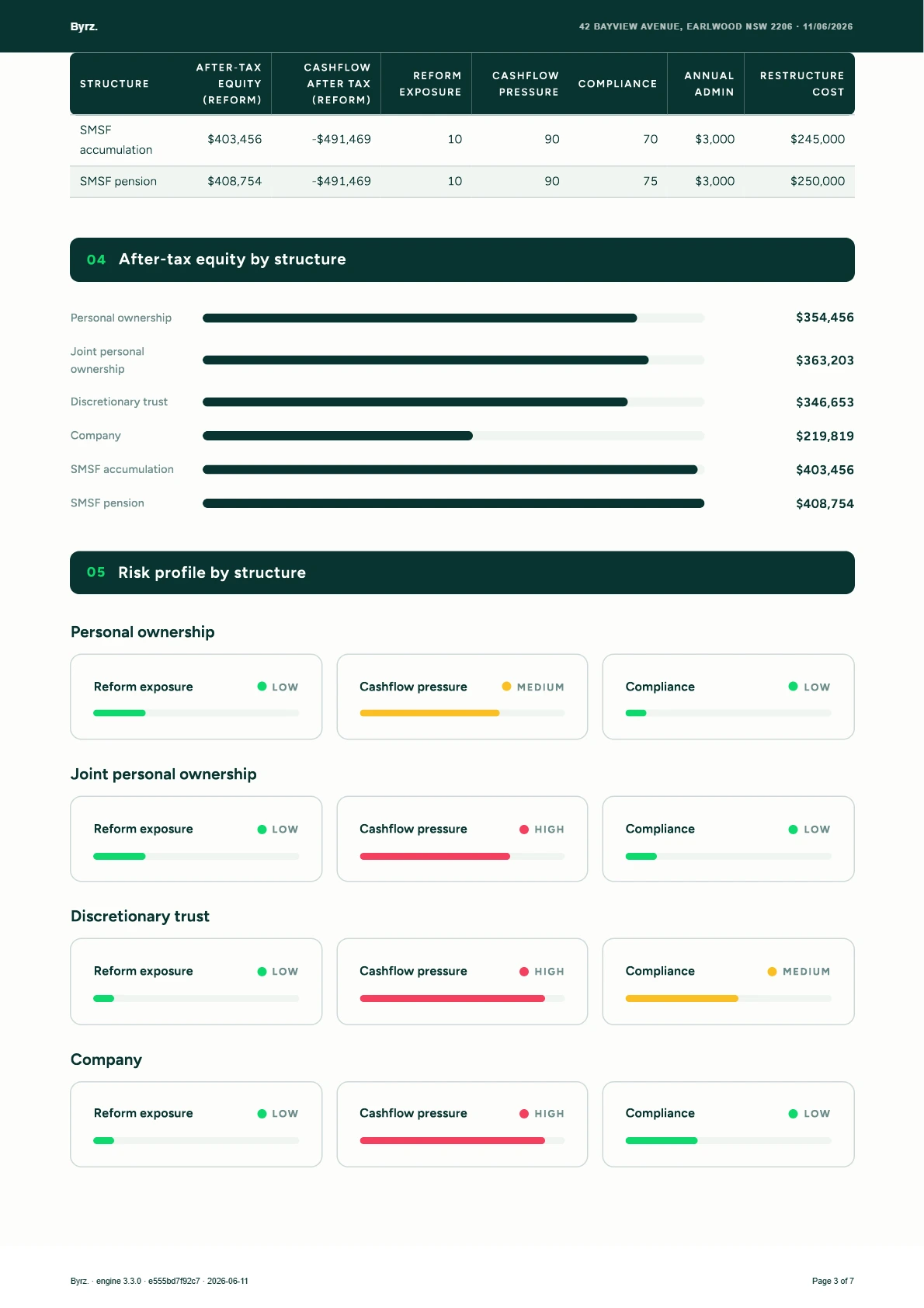

Structure comparison

Personal, trust, company or super? Model it before you commit.

Personal ownership

One owner, direct marginal-rate exposure.

Joint personal ownership

Two owners, split by ownership percentages.

Discretionary trust

Trust distributions plus the proposed 30% minimum-tax floor from 2028-29.

Company

Retained earnings, no 50% CGT discount, optional franking at sale.

SMSF accumulation

Pre-pension super fund. Earnings taxed at 15%, long-term gains 10% effective.

SMSF pension

Retirement-phase super fund. Eligible income and gains taxed at 0%. Div 296 modelled when TSB > $3M.

Sell timing

Should you sell before the rules change, or hold longer?

Sell timing can change projected value, CGT exposure, cashflow pressure and after-tax equity. One property report includes two sell dates so you can compare an earlier exit against a longer-hold scenario.

Sell date A

Earlier sale scenario

Model selling before the proposed reform start, for example 30 June 2027.

Sell date B

Longer hold scenario

Model holding beyond the reform start, for example a 2032 sale.

Delta view

Compare side-by-side

See the CGT, total tax, after-tax equity and cashflow difference between the two sell dates for your chosen structure.

Pricing

Choose your report credits.

You are not paying per structure. One property report can compare personal, joint, trust, company and SMSF outcomes, plus two sell dates. You currently have 0 report credits on this email.

Report credits are linked to your email, so you can access them after purchase.

Single Report

Best for one property decision.

1 property report

- 1 property report

- 2 sell dates

- Compare up to 6 ownership structures

- PDF + CSV export

- Adviser checklist

Investor Pack

Best for active investors comparing multiple properties.

3 property reports

- 3 property reports

- Compare multiple properties

- New build vs established scenarios

- Sell timing comparison

- PDF + CSV exports

Adviser Pack

Best value$299 / 20 reports

Best for accountants, brokers, buyers agents and property advisers.

20 property reports

- 20 property reports (~$15 each)

- Client-ready PDFs to forward

- Priority access to new structure types

- Direct line to the team for feedback

- PDF + CSV exports

Checkout opens in Stripe. After payment you come back here with credits ready to spend on any property report.

You are purchasing report credits, not tax advice. Each report is an estimate only and should be reviewed with a qualified adviser.

Digital report-generation product. Refunds are generally not available once a report has been generated, except where required by law or where a technical issue prevents generation.

Report scope

What counts as one property report?

One property report covers one asset or proposed purchase. You can compare multiple ownership structures inside that report, including personal ownership, joint ownership, discretionary trust, company, SMSF accumulation and SMSF pension. You only need another report credit when you want to model a different property, different address, different proposed purchase, or materially different deal.

Included in one report

- Personal vs trust vs SMSF comparison

- Sale year sensitivity

- Two-sell-date comparison for the same property

- Growth assumption changes before final export

- New build vs established flag for that same property

- PDF and CSV export

Needs another report

- Different property

- Different address

- Different purchase opportunity

- Different asset class

- Separate client report

Sample report

A clear PDF you can read in one sitting.

The PDF is built to be read on its own. Every number includes the assumption behind it, statutory references where they bite, and the questions worth answering before signing a contract or restructuring ownership. Forward it to an accountant if you want a second opinion.

Example Investment Property

Illustrative numbers. Your report will differ.

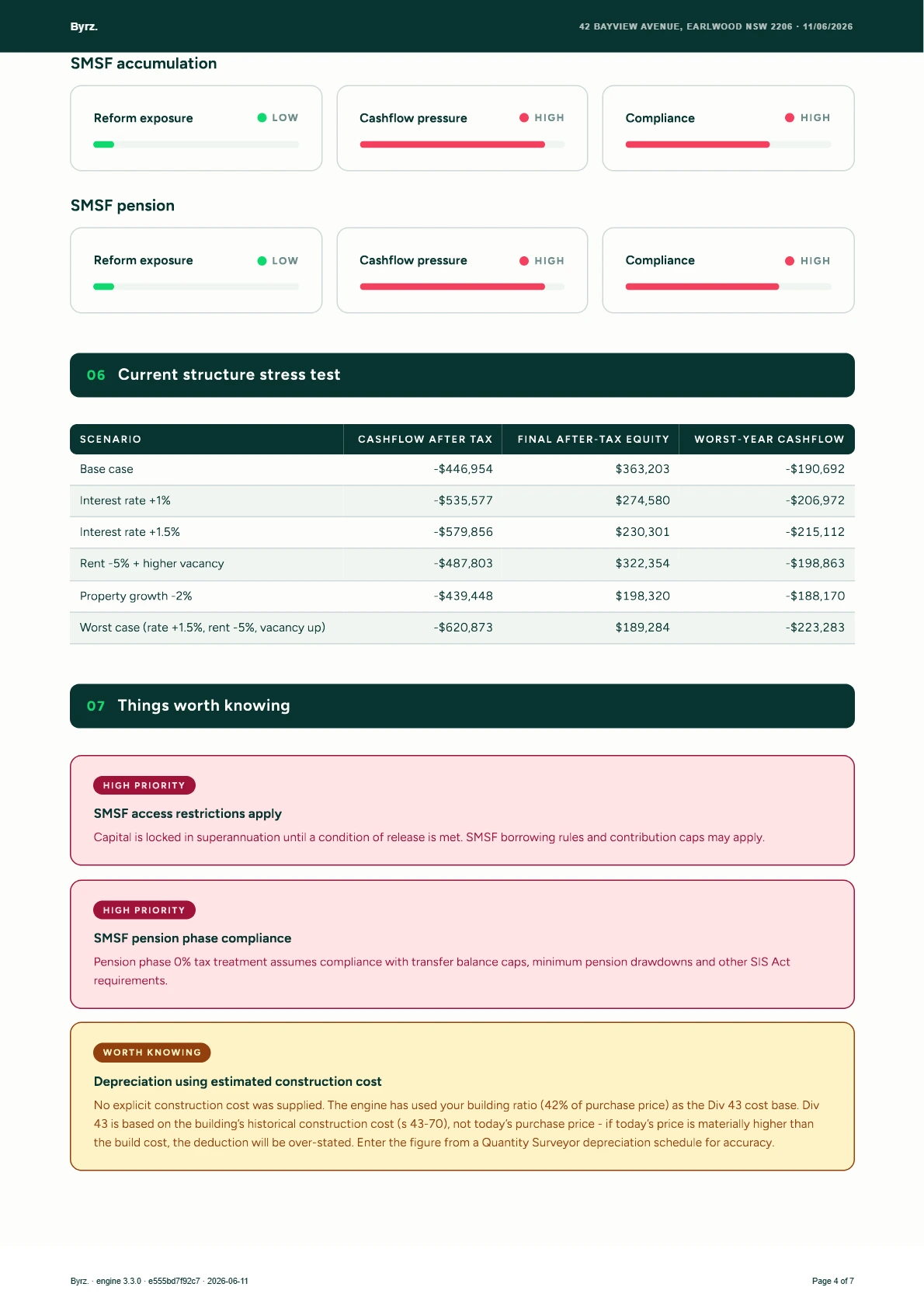

SMSF result is tax-efficient under assumptions but includes access, borrowing and compliance constraints.

How it works

Run the 2027 property tax reform on your property in minutes.

Enter property details

Purchase price, current value, loan, rent, expenses and the sell date.

Pick the structure

Analyse one, or switch to Compare mode for a side-by-side matrix across all six.

Adjust the forecast

Edit growth, rent growth, CPI and vacancy if the defaults don’t suit.

Unlock the report

Use 1 credit to unlock the full PDF, CSV or JSON. Read it yourself, or share with an accountant.

FAQ

Clear answers. No fine-print games.

Start your Tax Reform Impact Report

One property. Multiple structures. Two sell dates. Built to prepare better questions before you buy, sell, hold or restructure.

ownership structures you can model

sell dates compared per property

Keep reading

Understand the 2027 property tax reform

Official sources